How VIX 1D Helped Me Design a 0DTE Strategy

My latest research on creating a rules-based 0DTE SPX strategy using VIX 1D and S&P500 intraday patterns.

11/13/20252 min read

How I’m Developing a Systematic Strategy for Trading 0DTE Options

In this short article, I’d like to share my latest research on how I plan to approach trading 0-day-to-expiration (0DTE) options.

I traded them in the past, but eventually stopped for two reasons:

the results were mixed, and

I didn’t have a proper system in place.

As a quant, the second issue bothered me the most. I need defined rules so I know what to expect. Unfortunately, for 0DTEs there isn’t much literature to draw from—until one day, while showering, I started thinking about the VIX 1D.

The VIX 1D is essentially the VIX, but computed using options expiring in one day instead of thirty. That alone makes it an interesting tool for building intraday systems.

A Surprising Observation About VIX 1D

Before even running the analysis, I noticed something striking:

In 97% of cases, VIX 1D opens negative.

In 89% of cases, it moves from negative to positive from open to close.

This is statistically meaningful.

If your idea is to sell iron condors before the close to profit from an overnight volatility crush, I would be cautious. While volatility may fall, price can move significantly overnight—and that movement can easily offset the volatility gain.

Given that VIX 1D tends to rise from open to close, one could argue that systematically opening calendar spreads might work, since these benefit from rising volatility.

The problem? The S&P 500 often moves intraday. If the price moves too far, even a volatility increase won’t save a calendar spread.

Finding a Better Signal

To get around this, I looked for a relationship between:

The S&P 500’s open-to-close price move, and

What VIX 1D does at the open.

There was a correlation—good news.

And what does the math say?

The signal can justify going both long and short depending on the opening conditions.

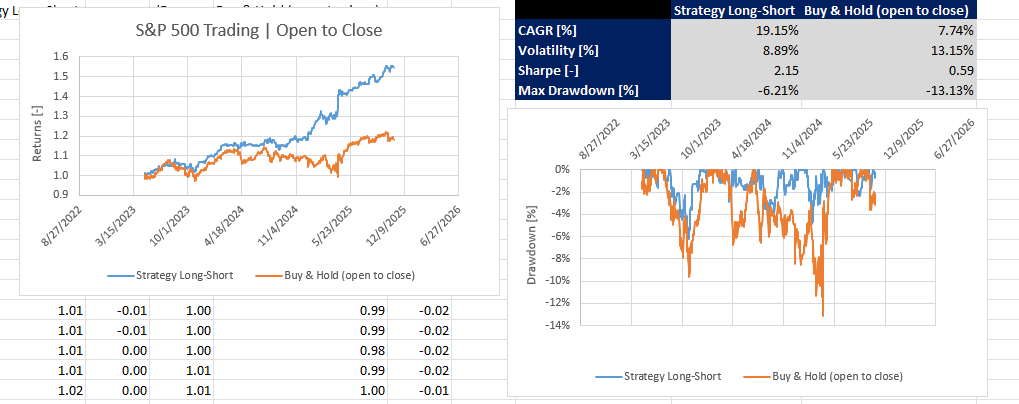

The chart below compares this strategy with a simple “buy SPY at the open, sell at the close” approach.

Even on a risk-adjusted basis, performance looks decent.

The simulation starts in April 2023, which is when VIX 1D data becomes available.

So What Does This Have to Do With 0DTE Options?

The current implementation is straightforward:

If the signal at the open says go long, I open an ATM bull vertical.

If the signal says go short, I open an ATM bear vertical.

If the signal says stay in cash, I plan to use a calendar spread.

For now, I am “testing the waters” for a few months to validate whether the system behaves as expected.

If it does, I’ll allocate more capital.

If it doesn’t, I’ll refine it—0DTE trading has potential, but it absolutely requires a system. The options market is simply too efficient to trade blindly.

I’ll keep everyone updated as the research progresses.