Compounding and Consistency: The Mathematics Behind Real Wealth

This article shows how combining compounding with regular contributions—weekly, monthly, or even annually—dramatically changes long-term investment results. Using 30 years of SPY data, it compares multiple contribution frequencies and shows why timing matters far less than disciplined, repeated investing.

11/18/20252 min read

Often we hear the expression that compounding is the 8th wonder of the universe.

Yes, it is — but why?

Because compounding quietly does something the human brain is terrible at understanding:

it turns time into an exponential multiplier.

Most things in life grow linearly — effort in, result out.

But compounding flips the logic: past gains start generating new gains, which then produce more gains, and so on. The growth stops being proportional to the effort and becomes proportional to the total accumulated base.

That is why a small difference in return or time becomes massive over long horizons.

That is why early action beats perfect action.

That is why patience outperforms brilliance.

Compounding is the 8th wonder not because it is complicated,

but because it quietly bends the rules of growth in your favor — if you give it enough time.

To further amplifying gains many traders and investors combine compounding with dollar cost averaging. Why is this?

Dollar-Cost Averaging (DCA) is a simple investment technique where you invest a fixed amount of money at regular intervals — for example, every week or every month — regardless of the market price.

When prices are high, your fixed amount buys fewer units.

When prices are low, the same amount buys more units.

Over time, this smooths out the average purchase cost and reduces the impact of bad timing.

Returns are exponentially amplified.

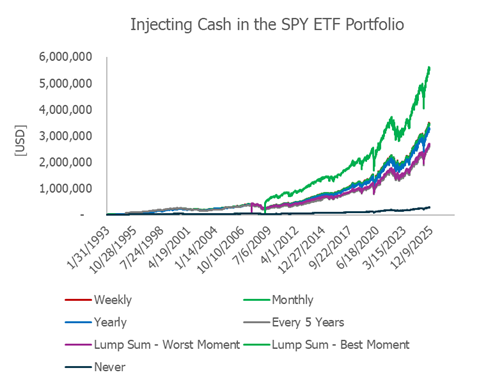

How much can consistency and timing really change the outcome?

Let’s walk through a simple example.

Imagine starting with $10,000 invested in SPY (the S&P 500 ETF) at its launch in 1993.

Then imagine adding $12,000 every year, for a total of $393,190 contributed over the entire period.

A common question I get is:

“How often should I add money? Weekly? Monthly? Once a year?”

Frequency matters — a lot.

To illustrate this, I compared six scenarios using the same total amount invested:

Weekly contributions

Monthly contributions

Yearly contributions

One lump-sum every 5 years

A perfect investment at the bottom of the 2007–2009 crisis

A terrible investment at the market peak right before that crisis

The results are striking.

Yes — if you perfectly catch the bottom of a recession, your returns explode.

But in real life, no one knows where the bottom is.

What surprised me was that even investing at the absolute peak before the Great Financial Crisis, given enough time (around 20+ years), the long-run outcome is not catastrophic. Not optimal — but not disastrous either.

So what’s the best frequency, since we can’t time the market?

Weekly and monthly contributions consistently outperform.

Annual or once-every-five-years contributions lag meaningfully behind.

Here’s the most interesting part:

We started with $10,000, added a total of $393,190, and after roughly 30 years the portfolio grew to more than $3,000,000.

If we had not contributed regularly, the final value would have been only $276,366.

In the end, wealth isn’t built through brilliance or perfect timing — it’s built through discipline.

Small, steady contributions combined with compounding create results that look impossible at the beginning and inevitable at the end.