Investment Methodology & Risk Framework

The Architecture of Alpha: From Derivative Signals to Systematic Execution

At MVK Alpha Capital, we do not rely on subjective market "narratives." Our investment process is built on a rigorous, quantitative framework that translates complex derivative market signals into actionable, risk-adjusted portfolios.

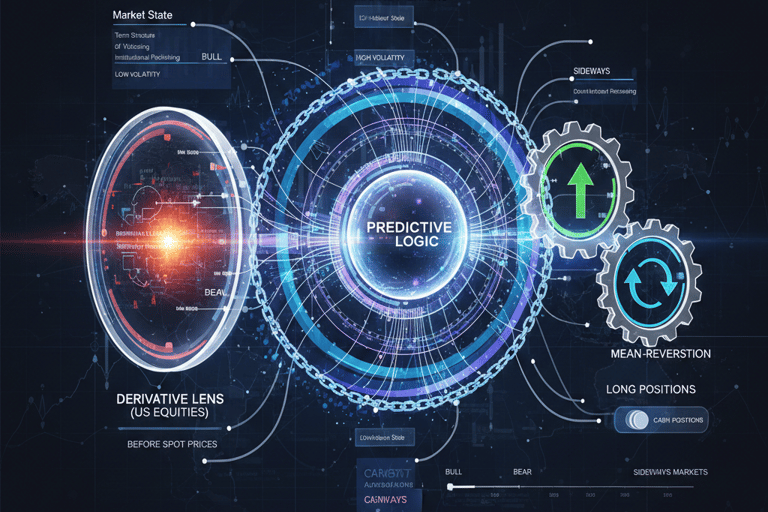

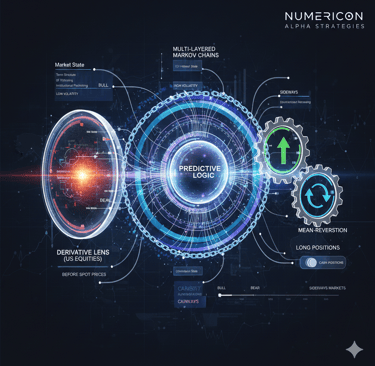

1. The Core Engine: Predictive Logic

Numericon Alpha strategies are governed by high-dimensional statistical models designed to navigate shifting market regimes.

Multi-Layered Markov Chains: Unlike linear models, our strategies utilize multi-layered Markov Chains. This allows the system to identify the current "Market State" (Regime) and calculate the transition probabilities of moving into a different volatility or price environment.

Predictive Inputs (The Derivative Lens): We use the US Equities Derivative Market as our primary predictor. By analyzing the term structure of volatility, our models detect institutional positioning and "smart money" movements before they are reflected in spot prices.

Momentum & Mean-Reversion: Depending on the detected state, the system toggles between long and cash positionst, ensuring the strategy remains relevant across bull, bear, and sideways markets.

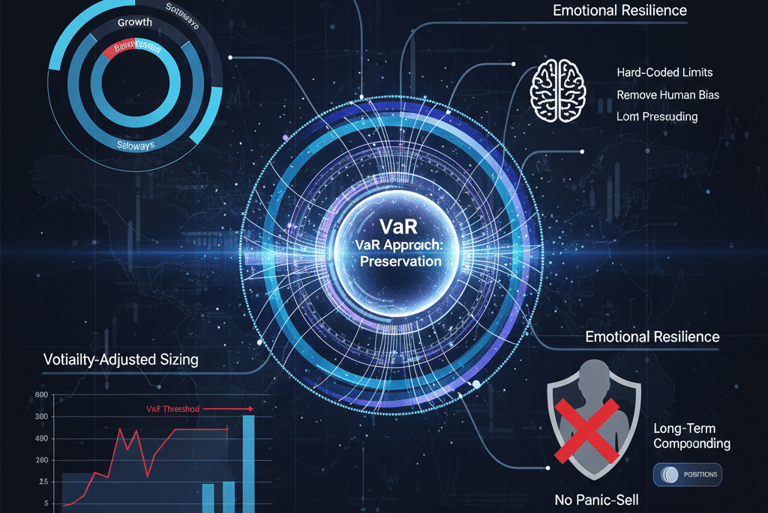

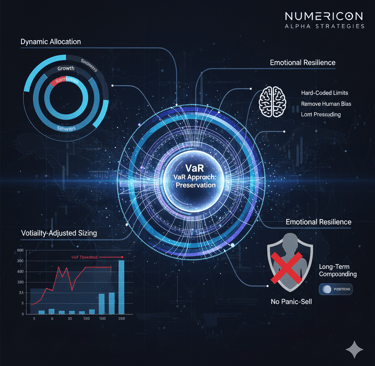

2. Risk Management: The VaR Approach

The cornerstone of our capital preservation strategy is the Value at Risk (VaR) framework. We believe that professional investing is as much about managing "Emotional Pain" as it is about managing capital.

Dynamic Allocation: For both Numericon Alpha and our Growth/Balanced/Preservation models, we use a VaR-based approach to determine asset weights.

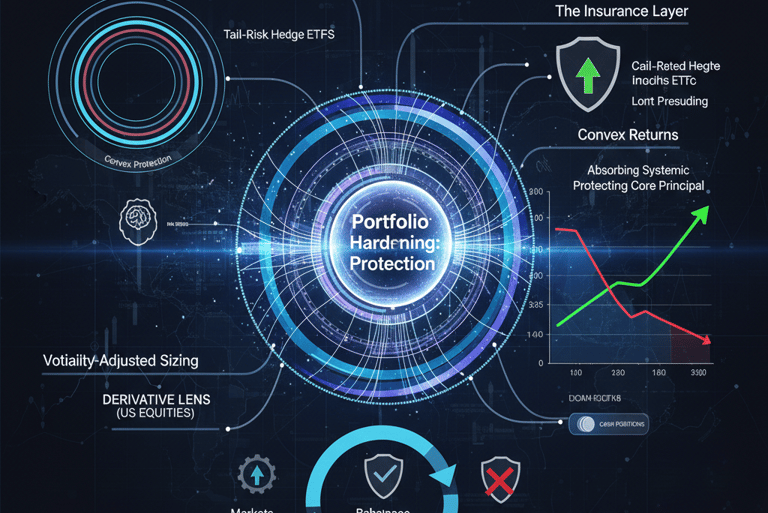

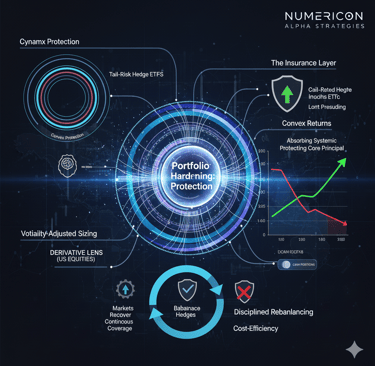

Volatility-Adjusted Sizing: When market volatility increases, the VaR threshold triggers an automatic reduction in position sizing for certain assets. This ensures that the potential "worst-case" daily loss remains within pre-defined, tolerable limits for the client.

Emotional Resilience: By hard-coding these limits, we remove human bias and the temptation to "panic-sell" during high-volatility events, keeping the long-term compounding engine intact.

3. Portfolio Hardening: Tail-Risk Protection

While VaR manages daily fluctuations, we implement a secondary layer of defense to protect against "Black Swan" events—the extreme market crashes that traditional models often ignore.

Convex Protection: For the Numericon Growth, Balanced, and Preservation models, we integrate dedicated Tail-Risk Hedge ETFs.

The Insurance Layer: These instruments are designed to provide explosive, convex returns during severe market drawdowns. This "insurance policy" acts as a counter-weight, absorbing the impact of sudden systemic shocks and protecting the core principal of the portfolio.

Disciplined Rebalancing: As markets recover, the framework rebalances these hedges to ensure cost-efficiency and continuous coverage.

4. Operational Infrastructure

Execution: Fully automated via Python-based algorithms.

Custody: Strategies are deployed directly within the client’s Interactive Brokers (IBKR) or Exante account, ensuring maximum transparency and liquidity.

Precision: Real-time monitoring ensures that every trade is executed with minimal slippage and strict adherence to the underlying quantitative model.

Ready to see our methodology in action?

Contact Us.