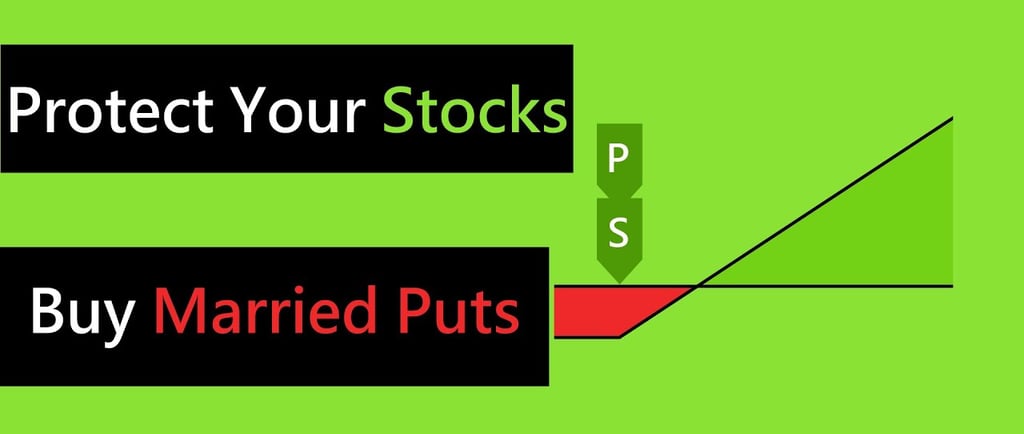

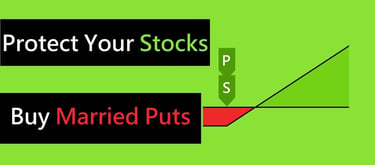

Protecting Your Portfolio: The Role of Married Puts in Volatile Markets

Discover the power of married puts as a hedging strategy to shield your equity portfolio from severe market downturns. Using the S&P 500 ETF (SPY) as a practical case study, this article delves into the challenges of volatile markets, explains the mechanics of married puts, and provides expert rules for implementation and management to foster resilient, disciplined investing.

9/11/20253 min read

In the unpredictable world of investing, safeguarding capital during downturns is paramount. This article explores married puts as a strategic hedge, using the S&P 500 ETF (SPY) as a case study to illustrate their application and management.

The Challenge: Navigating Market Drawdowns

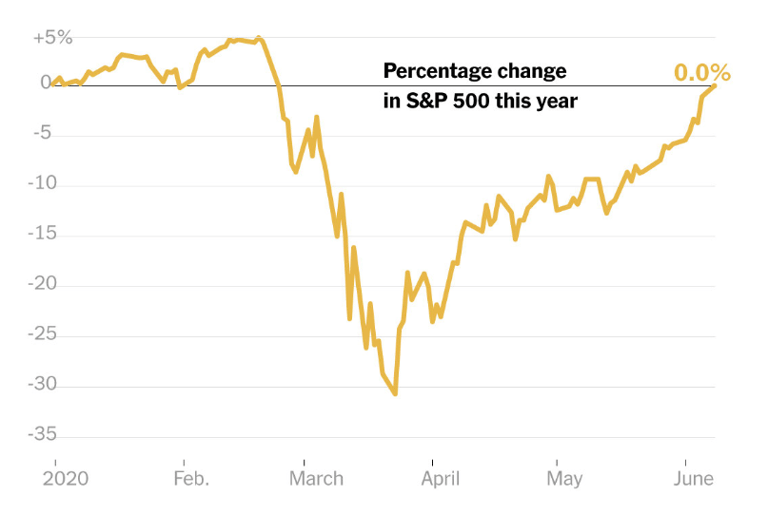

Many investors allocate significant capital to equities, such as holdings in SPY, which tracks the S&P 500 index. However, sharp market declines, such as the April 2025 correction or the COVID-19 crash in 2020, can lead to portfolio drawdowns of 20-30%. These events often trigger emotional responses: investors may sell at lows, locking in losses, or make impulsive decisions that compound the damage. Historically, markets tend to rebound after such dips, leaving panicked sellers on the sidelines and regretting missed recoveries. The core issue is protecting against downside risk without abandoning long-term growth potential. Married puts offer a structured solution to mitigate this volatility and preserve investor composure.

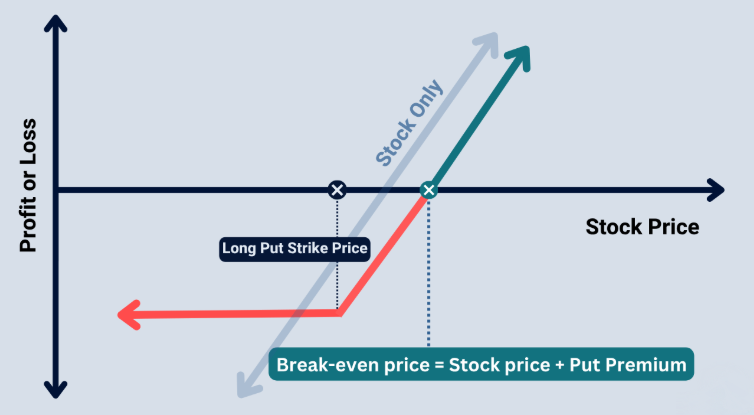

Understanding Married Puts: A Protective Strategy

A married put is an options strategy where an investor holds a long position in an underlying asset, such as shares of SPY, and simultaneously purchases put options on the same asset to hedge against declines. The "married" aspect refers to the puts being bought in tandem with the stock position, effectively creating a floor below which losses are limited.

In application to SPY, consider an investor with 1,000 shares at a current price of $650 (spot price). To implement a married put, they would buy 10 put contracts (since each contract covers 100 shares, matching the equity exposure via the multiplier of 100). The put provides the right to sell SPY at a predetermined strike price, insuring the portfolio against falls below that level. This strategy acts like portfolio insurance: if SPY drops sharply, the put's value rises, offsetting equity losses. However, it comes at the cost of the put's premium, which erodes if the market rises or remains stable.

Practical Implementation and Management Rules

Drawing from nearly a decade of experience in asset management, effective use of married puts on SPY hinges on disciplined rules. Investors' typical pain threshold is around a 10% drawdown, beyond which behavioral biases intensify.

Initial Setup:

Select a strike price at 90% of the current SPY spot price (e.g., if SPY is $650, choose a $585 strike).

Purchase puts proportional to your equity exposure, accounting for the 100-share multiplier.

Opt for puts with approximately 90 days to expiration (DTE) to balance cost and protection without excessive time decay.

Ongoing Management:

Rally Scenario: If SPY rises (e.g., 2-3% or more), adjust by rolling the put to a new strike 10% below the updated spot price, maintaining the hedge.

Stable Market: If uneventful, roll the contract forward to restore 90 DTE, avoiding accelerated Theta decay and high Vega in shorter-dated options.

Drawdown Scenario (e.g., 20% drop or more): Your portfolio is cushioned, down only about 10% net of the put's gain. Two paths forward:

1. Conservative Approach: Hold steady. Roll puts as needed, but always set strikes 10% below SPY's all-time high to preserve protection without over-hedging.

2. Opportunistic Approach: Capitalize on dips without market-timing signals.

a. Maintain the base hedge, but for every additional 5% decline in SPY, allocate 0.5-1% of assets under management (AUM) to at-the-money (ATM) bull call vertical spreads. Ladder these positions: profits accrue on recoveries, while losses are contained if declines persist. Cease additions once SPY rebounds above 10% below its all-time high.

b. Use the proceeds to purchase additional SPY shares at the lower price. This reduces the portfolio’s average cost basis, amplifying returns during a recovery. For example, $12,000 from put sales could buy 30 shares at $400, enhancing gains if SPY rebounds to $500, while new puts are established to maintain protection at a strike 10% below the all-time high.

The annual cost of this protection is approximately 4%, which may seem substantial but proves invaluable during meltdowns, averting emotional pitfalls. Advanced variations of this married put strategy, can reduce expenses but warrant separate article.

By integrating married puts, investors can endure volatility with greater resilience, transforming potential crises into manageable events. This approach, when applied judiciously to SPY, fosters disciplined decision-making in any market environment.