The Growing Risk of a Global Liquidity Crisis

Global debt is growing faster than the world’s economies can handle. The result could be a severe liquidity crunch that reshapes the global markets.

10/16/20252 min read

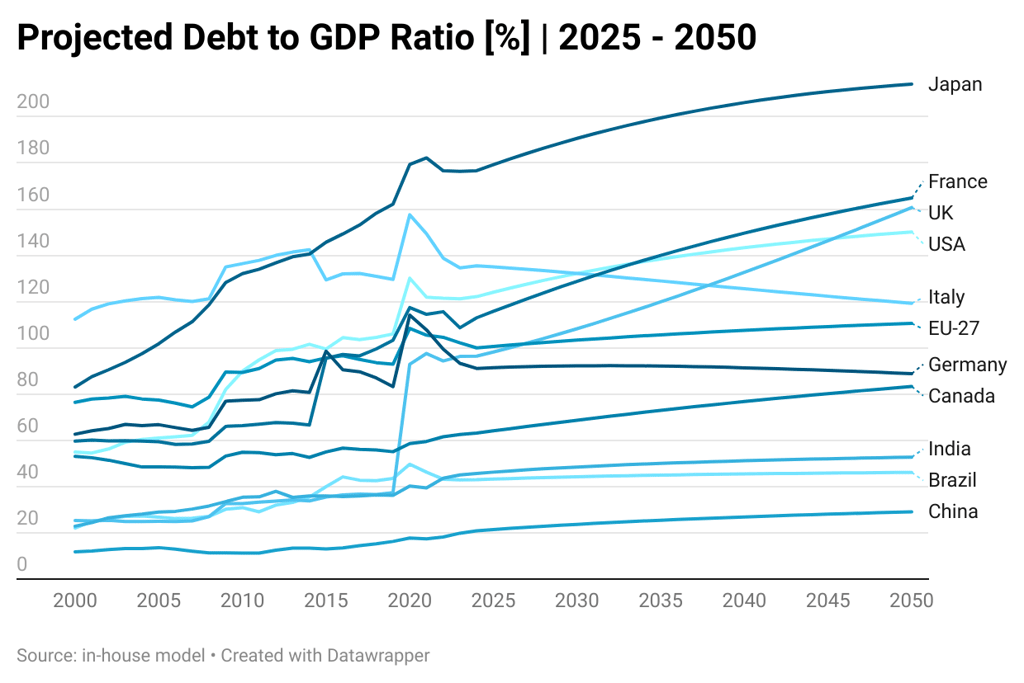

A compelling—though blurred—chart recently caught my attention. Its message is clear: in the years ahead, global liquidity could tighten dramatically as debt growth outpaces GDP growth across major economies.

The Core of the Problem: This debate often revolves around the United States, given its massive debt levels. But when viewed in relative terms—debt compared to the size of the economy—countries like the UK, Japan, and France look equally or even more vulnerable.

France’s situation is particularly delicate: it cannot “print its way out” of trouble since it shares the euro. The UK, Japan, and the US technically can, but excessive money creation risks stoking inflation, not solving the underlying problem.

Why the Assumptions Are Optimistic: The projections presented in this article assume that both GDP and debt will continue to grow at the same pace as in the past two decades. That’s a generous assumption. In countries like the UK and France, open-border policies combined with undifferentiated welfare spending add strain without necessarily increasing productivity.

In the US, much depends on the success—or failure—of the current administration’s economic policies.

Lessons from 2008: If you remember the 2007–2009 financial crisis, imagine something broader.

A global liquidity crunch could be far worse—an event where printing more money only fuels additional inflation in an already contracting economy. Europe seems particularly exposed, with France potentially being the first domino to fall.

Early Warning Signs:

Bond yields in France, Germany, and the UK have soared over the past year—an indication that investors now demand a higher risk premium.

Gold prices are surging, reflecting a flight to safety as confidence in fiat currencies wanes.

Ironically, Italy, long considered fragile, appears relatively stable—for now.

How Investors Might Capitalize: Getting the direction right is not enough — if the timing is wrong, it’s still a losing trade. Liquidity crises can take months or even years to unfold, and positioning too early can be as costly as being wrong altogether.

A more balanced approach involves using options to express views while limiting downside risk, and hard assets to hedge against inflation and currency devaluation.

Some possible approaches:

Protective options strategies — such as long puts on equity indexes or call spreads on volatility products — can offer asymmetric upside if markets break down.

Short exposure to European sovereign bonds (via ETFs or futures) could profit as yields climb and credit risk rises.

Allocations to hard assets — especially gold and silver — provide a store of value if fiat currencies weaken.

Selective exposure to quality U.S. equities with low leverage and strong cash flows can help preserve purchasing power during tightening cycles.

In short, stay directionally aware but tactically flexible — liquidity shocks reward patience and punish premature conviction.